Medicare helps over 65 million Americans get access to healthcare once they reach retirement age. Most assume turning 65 is the magic ticket that guarantees coverage. But almost every year, thousands learn that not meeting the right work or residency rules can leave them paying hundreds extra for the same care. Understanding how these eligibility rules really work can reshape how you plan for your future.

Table of Contents

Quick Summary

| Takeaway | Explanation |

|---|

| Medicare is for those aged 65+ | Most individuals qualify for Medicare when they reach 65 years of age, ensuring coverage for seniors. |

| Work history impacts coverage | To receive premium-free Part A, you must have paid Medicare taxes for about 10 years through employment. |

| Special cases allow earlier access | Individuals under 65 can qualify for Medicare if they receive Social Security disability benefits or have specific medical conditions like ESRD or ALS. |

| Understand enrollment periods | The Initial Enrollment Period spans seven months around your 65th birthday, crucial for avoiding penalties. |

| Limited dental and vision coverage | Original Medicare has significant gaps in dental and vision care; consider Medicare Advantage or supplemental plans for better coverage. |

What Are Medicare Eligibility Requirements?

Medicare eligibility requirements are specific guidelines that determine who can enroll in this critical federal health insurance program. Understanding these requirements helps individuals plan for their healthcare needs as they approach retirement age.

Age and Citizenship Criteria

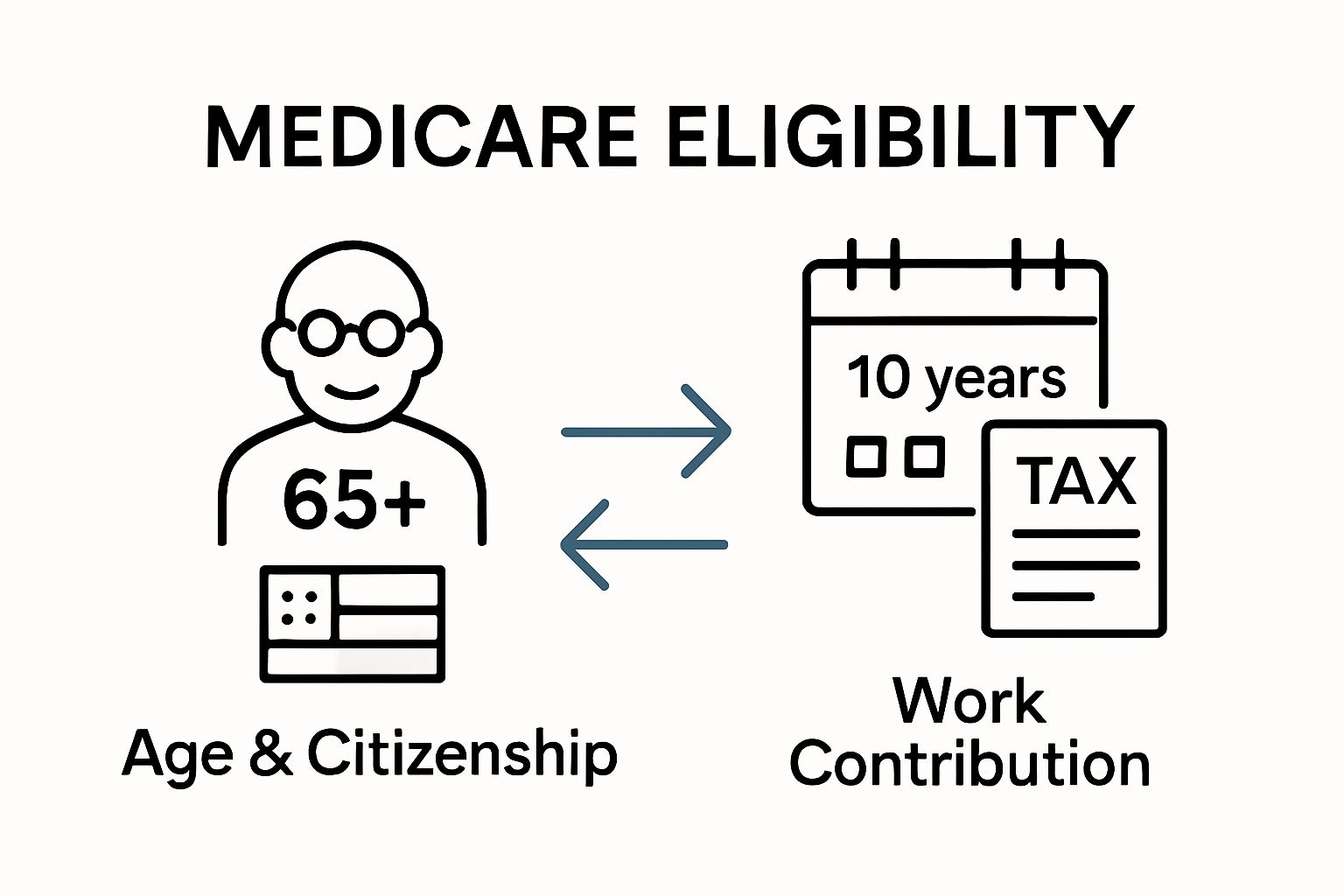

The primary medicare eligibility requirements center around two fundamental factors: age and citizenship status.

Most individuals become eligible for Medicare when they turn 65 years old. To qualify, you must be a United States citizen or a permanent legal resident who has lived in the country for at least five continuous years.

According to the Social Security Administration, this foundational requirement ensures that long-term contributors to the U.S. healthcare system can access essential medical coverage. Key citizenship and age requirements include:

- U.S. citizenship or legal permanent residency

- Minimum age of 65 years old

- Continuous U.S. residency for at least five years

Work History and Contribution Factors

Beyond age and citizenship, your work history plays a crucial role in Medicare eligibility. Individuals who have paid Medicare taxes for approximately 10 years through their employment typically qualify for premium-free Part A hospital insurance. This means that if you or your spouse worked and paid Medicare taxes for a sufficient duration, you can access basic Medicare coverage without additional monthly premiums. For those who haven’t met the full work history requirements, alternative enrollment options exist. You might be eligible to purchase Medicare coverage by paying monthly premiums.

Learn more about Medicare enrollment options and understand how your specific work history impacts your potential coverage. Additional scenarios that can influence Medicare eligibility include receiving Social Security disability benefits for 24 months or having specific medical conditions like End-Stage Renal Disease (ESRD) or ALS. These special circumstances can enable individuals under 65 to access Medicare benefits earlier than the standard retirement age.

Why Medicare Eligibility Matters for Seniors

Medicare eligibility represents far more than a bureaucratic milestone. It signifies a critical transition in healthcare access, financial protection, and personal wellness for millions of older Americans. Understanding why Medicare matters goes beyond simple enrollment requirements.

Healthcare Access and Financial Protection

Medicare provides a fundamental safety net for seniors, ensuring they can access essential medical services without facing devastating financial consequences.

Research from the National Institutes of Health demonstrates that Medicare coverage significantly reduces healthcare disparities among older adults, particularly for those with limited economic resources. The financial implications of Medicare are substantial:

- Comprehensive medical coverage without high individual expenses

- Protection against catastrophic healthcare costs

- Access to preventive services often unavailable without insurance

Long-Term Health Management

Beyond immediate medical needs, Medicare eligibility enables seniors to proactively manage their long-term health. The program covers a wide range of services including hospital stays, physician visits, preventive screenings, and specialized treatments that become increasingly important with age.

Learn more about comprehensive Medicare coverage options, which can help you navigate the complex landscape of senior healthcare. Specialized Medicare programs recognize that healthcare needs evolve. Different parts of Medicare address various aspects of medical care, from hospital stays to prescription medications, ensuring seniors receive comprehensive support tailored to their changing health requirements.

Quality of Life Considerations

Medicare eligibility is not just about medical treatments but about maintaining independence and dignity during retirement years. By providing reliable, affordable healthcare coverage, Medicare allows seniors to focus on enjoying their lives rather than worrying about potential medical expenses. The program supports seniors in maintaining their quality of life, accessing necessary treatments, and preserving their financial stability during a vulnerable period of life.

Key Groups Eligible for Medicare Coverage

Medicare coverage extends beyond the traditional understanding of senior healthcare, encompassing several unique groups with specific eligibility criteria. Understanding these diverse categories helps individuals recognize their potential access to this critical federal health insurance program.

Standard Retirement Age Group

The most common Medicare eligibility group consists of individuals aged 65 and older. These individuals typically qualify automatically if they or their spouse have worked and paid Medicare taxes for approximately 10 years. According to the Centers for Medicare & Medicaid Services, this primary group represents the core population for Medicare enrollment. Key characteristics of the standard retirement age group include:

- U.S. citizens or permanent residents

- Minimum age of 65 years

- Sufficient work history with Medicare tax contributions

Special Disability and Medical Condition Groups

Medicare eligibility is not exclusively tied to age.

Certain individuals under 65 can qualify through specific disability or medical conditions. People receiving Social Security Disability Insurance (SSDI) for 24 consecutive months automatically become eligible for Medicare, regardless of their age.

Explore more about Medicare Advantage options that cater to these unique enrollment scenarios. Special groups with early Medicare access include:

- Individuals with End-Stage Renal Disease (ESRD)

- People diagnosed with Amyotrophic Lateral Sclerosis (ALS)

- Long-term Social Security Disability Insurance recipients

Specific Healthcare Condition Categories

Some Medicare eligibility pathways are defined by specific healthcare conditions that transcend typical age or disability requirements. Individuals with permanent kidney failure requiring dialysis or kidney transplant automatically qualify for Medicare, irrespective of age. Similarly, those diagnosed with ALS receive immediate Medicare coverage without the standard 24-month waiting period. These specialized eligibility paths demonstrate Medicare’s commitment to supporting vulnerable populations, ensuring critical medical coverage for those facing significant health challenges. To help clarify who may qualify for Medicare, the following table summarizes the primary eligibility categories and their main criteria.

| Eligibility Group | Main Age Requirement | Key Criteria | Example Conditions |

|---|

| Standard Retirement Age Group | 65 or older | U.S. citizen/permanent resident; 10 years Medicare taxes | Retirees meeting residency & work rules |

| Social Security Disability Recipients | Under 65 | 24 months of Social Security Disability Insurance (SSDI) | Disabled before age 65 |

| End-Stage Renal Disease (ESRD) Patients | Any age | Permanent kidney failure, requires dialysis/transplant | Diagnosed with ESRD |

| ALS (Lou Gehrig’s Disease) Patients | Any age | ALS diagnosis; immediate eligibility | Diagnosed with ALS |

| Non-Qualifying Work History or Recent Residents | 65 or older | Not enough work history; may pay monthly premiums | Recent immigrants; spouses without work |

| The program’s flexibility reflects a nuanced approach to healthcare access, recognizing that medical needs do not conform to a one-size-fits-all framework. | | | |

Understanding Enrollment Periods for Medicare

Medicare enrollment periods are complex scheduling windows that determine when and how individuals can sign up for health coverage. These strategic timeframes are designed to help people transition smoothly into Medicare while providing flexibility for unique personal circumstances.

Initial Enrollment Period

The Initial Enrollment Period represents the primary window for Medicare signup.

According to the Centers for Medicare and Medicaid Services, this critical timeframe begins three months before an individual turns 65 and extends three months after their 65th birthday. During these seven total months, individuals can enroll without facing potential penalties or coverage gaps. Key components of the Initial Enrollment Period include:

- Automatic signup for those receiving Social Security benefits

- Option to delay enrollment without penalties under specific conditions

- Comprehensive window to select preferred Medicare plan options

Special Enrollment Periods

Not all Medicare enrollment follows standard timelines.

Special Enrollment Periods provide alternative signup opportunities for individuals experiencing significant life changes.

Learn more about Medicare Advantage enrollment strategies to understand these unique scenarios. Special circumstances triggering alternative enrollment windows include:

- Losing current health insurance coverage

- Moving outside current plan’s service area

- Experiencing major life transitions like retirement

General Enrollment Period

For those who miss their initial and special enrollment periods, the General Enrollment Period offers a fallback option. Running from January 1 to March 31 each year, this window allows individuals to sign up for Medicare, though potential late enrollment penalties might apply. Coverage for those enrolling during this period typically begins on July 1 of the same year. Understanding these enrollment periods is crucial for avoiding coverage gaps and potential financial penalties. Medicare’s structured approach ensures that individuals have multiple opportunities to access essential healthcare coverage, recognizing that personal circumstances vary widely. The table below compares the three main Medicare enrollment periods to outline their eligibility windows, features, and potential consequences for missing deadlines.

| Enrollment Period | Timing & Duration | Who It Applies To | Key Features & Notes |

|---|

| Initial Enrollment Period | 3 months before to 3 months after 65th birthday (7 months total) | Anyone turning 65 | Avoids penalties; enroll with maximum plan choices |

| Special Enrollment Periods | Varies based on qualifying events | Those with job loss, relocation, or other specific situations | Opportunity outside standard window; triggered by life changes |

| General Enrollment Period | January 1 to March 31 annually | Anyone who missed previous periods | Late penalties may apply; coverage starts July 1 |

Impact of Medicare on Dental and Vision Needs

Medicare’s standard coverage presents significant limitations when it comes to dental and vision care, creating unique challenges for seniors seeking comprehensive healthcare. Understanding these coverage gaps is crucial for individuals planning their medical and financial strategies during retirement.

Standard Medicare Coverage Limitations

Original Medicare (Part A and Part B) provides minimal dental and vision benefits, primarily focusing on medically necessary treatments rather than routine care. According to the Centers for Medicare & Medicaid Services, most standard dental procedures and vision exams are not covered under traditional Medicare plans. Key coverage limitations include:

- No routine dental cleanings or preventive care

- Limited vision screening only during specific medical examinations

- Exclusion of standard eyeglasses and contact lens prescriptions

Medicare Advantage and Supplemental Options

Medicare Advantage plans offer more comprehensive dental and vision coverage, providing a potential solution to these standard coverage gaps.

Learn more about vision plan enrollment for seniors to understand alternative healthcare strategies. Additional coverage options for dental and vision care include:

- Medicare Advantage (Part C) plans with integrated dental and vision benefits

- Standalone dental and vision insurance supplements

- Discount programs specifically designed for seniors

Financial and Health Implications

The limitations in Medicare’s dental and vision coverage can lead to significant out-of-pocket expenses for seniors. Routine dental checkups, eye exams, and corrective eyewear are essential for maintaining overall health and detecting potential medical issues early. Seniors often find themselves navigating complex insurance landscapes to secure comprehensive care, requiring careful planning and potential additional investments in supplemental insurance.

These coverage challenges underscore the importance of proactive healthcare planning, encouraging seniors to explore multiple insurance options and understand the full spectrum of their potential medical needs during retirement.

Take the Confusion Out of Medicare Eligibility

Feeling uncertain about Medicare eligibility requirements? So many people struggle to understand the specifics around age, work history, and the right enrollment period. When you face complicated rules and fine print, making a decision about your health care can feel overwhelming. That confusion can lead to missed deadlines, unexpected costs, or gaps in coverage—exactly what you want to avoid.

Break through the clutter with support from trusted experts. Visit

GenerationHealth.me for truly clear step-by-step guidance, instant personalized quotes, and a library of answers tailored to your unique needs. Explore our dedicated

Medicare & Seniors-Insurance Agents section for advice built for people just like you. The sooner you get started, the sooner you can protect your health and your future. Compare your options, ask questions, and take control of your Medicare journey with confidence—start now and make Medicare simple.

Frequently Asked Questions

What are the basic Medicare eligibility requirements?

To be eligible for Medicare, you must be at least 65 years old, a U.S. citizen or a permanent legal resident who has lived in the U.S. for at least five continuous years.

How does my work history affect my Medicare eligibility?

If you’ve paid Medicare taxes for approximately 10 years, you typically qualify for premium-free Part A hospital insurance. If not, you may still qualify by paying monthly premiums.

Can individuals under 65 qualify for Medicare?

Yes, individuals under 65 can qualify for Medicare if they have received Social Security disability benefits for 24 months or have specific medical conditions like End-Stage Renal Disease (ESRD) or ALS.

What is the Initial Enrollment Period for Medicare?

The Initial Enrollment Period begins three months before you turn 65, extending three months after your 65th birthday. This seven-month window is crucial for enrolling in Medicare without incurring penalties.

Recommended