Nearly 15 million Americans choose ACA health insurance plans each year to secure affordable care for themselves and their families. Picking the right coverage can feel overwhelming, especially with so many rules and options. By learning what documents to prepare and how to compare key details, you can avoid surprises and make confident choices that support your specific health and financial needs.

Quick Summary

| Key Point | Explanation |

|---|---|

| 1. Gather all personal health details | Compile ID, income, and health info for each enrollee to streamline the application process. |

| 2. Understand your enrollment options | Explore both regular and special enrollment periods to find eligible plans suited to your needs. |

| 3. Compare premiums and benefits thoroughly | Analyze both costs and coverage options to ensure the plan meets your family’s healthcare requirements. |

| 4. Evaluate out-of-pocket expenses carefully | Assess total potential costs, including deductibles and network coverage, to avoid unexpected financial burdens. |

| 5. Confirm accuracy before enrollment | Double-check all provided information to ensure correct plan selection and avoid enrollment issues. |

Table of Contents

- Step 1: Gather Personal And Family Health Details

- Step 2: Identify Eligible ACA Plan Options

- Step 3: Compare Premiums, Coverage, And Benefits

- Step 4: Evaluate Out-Of-Pocket Costs And Networks

- Step 5: Confirm Plan Selection And Enrollment

Step 1: Gather personal and family health details

When shopping for ACA health insurance, your first critical task is collecting comprehensive personal and family health information. Think of this process like preparing for a strategic planning session where every detail matters.

Start by assembling key personal documents for each family member who will be enrolled. You will need specific identification and financial details including full legal names, birthdates, Social Security numbers, current home addresses, and citizenship or permanent residency status. According to research from the Kaiser Family Foundation, accurate demographic information is crucial for estimating potential healthcare subsidies and determining your exact coverage options.

Pay special attention to household income documentation. If you are hoping to qualify for premium tax credits or cost sharing reductions, you will need recent tax returns or current income statements. The Marketplace uses this information to calculate your potential financial assistance precisely.

Pro Tip: Gather documents for ALL potential enrollees beforehand to streamline your application process and prevent unexpected delays.

For families with complex health needs, compile additional information about current prescriptions, preferred healthcare providers, and any ongoing medical treatments. This will help you select a plan that matches your specific healthcare requirements. Explore our guide on family health insurance options for more detailed insights into matching plans with your unique situation.

Here’s a comparison of documents and information you should gather for ACA health insurance enrollment:

| Information Type | Required For All Applicants | Additional for Complex Needs |

|---|---|---|

| Full Legal Name | Yes | Yes |

| Date of Birth | Yes | Yes |

| Social Security Number | Yes | Yes |

| Home Address | Yes | Yes |

| Citizenship/Residency | Yes | Yes |

| Tax Returns/Income Proof | Yes | Yes |

| Prescription List | No | Yes |

| Current Providers | No | Yes |

| Ongoing Treatments | No | Yes |

Once you have collected these essential details, you will be fully prepared to move forward with comparing and selecting the right ACA health insurance plan for your family.

Step 2: Identify eligible ACA plan options

Now that you have gathered your personal details, the next step is understanding which health insurance plans are truly available for you. This stage is about discovering your specific coverage landscape and matching your family’s unique healthcare needs.

The Health Insurance Marketplace offers multiple pathways for finding eligible plans. According to research on health insurance enrollment, you have two primary enrollment windows: the standard open enrollment period and special enrollment periods triggered by significant life changes such as marriage, job loss, or having a child.

Start by exploring your state specific marketplace. Learn about your state’s ACA eligibility requirements to understand local nuances. Some states operate their own health insurance exchanges like Covered California or Access Health CT, which provide targeted options for local residents.

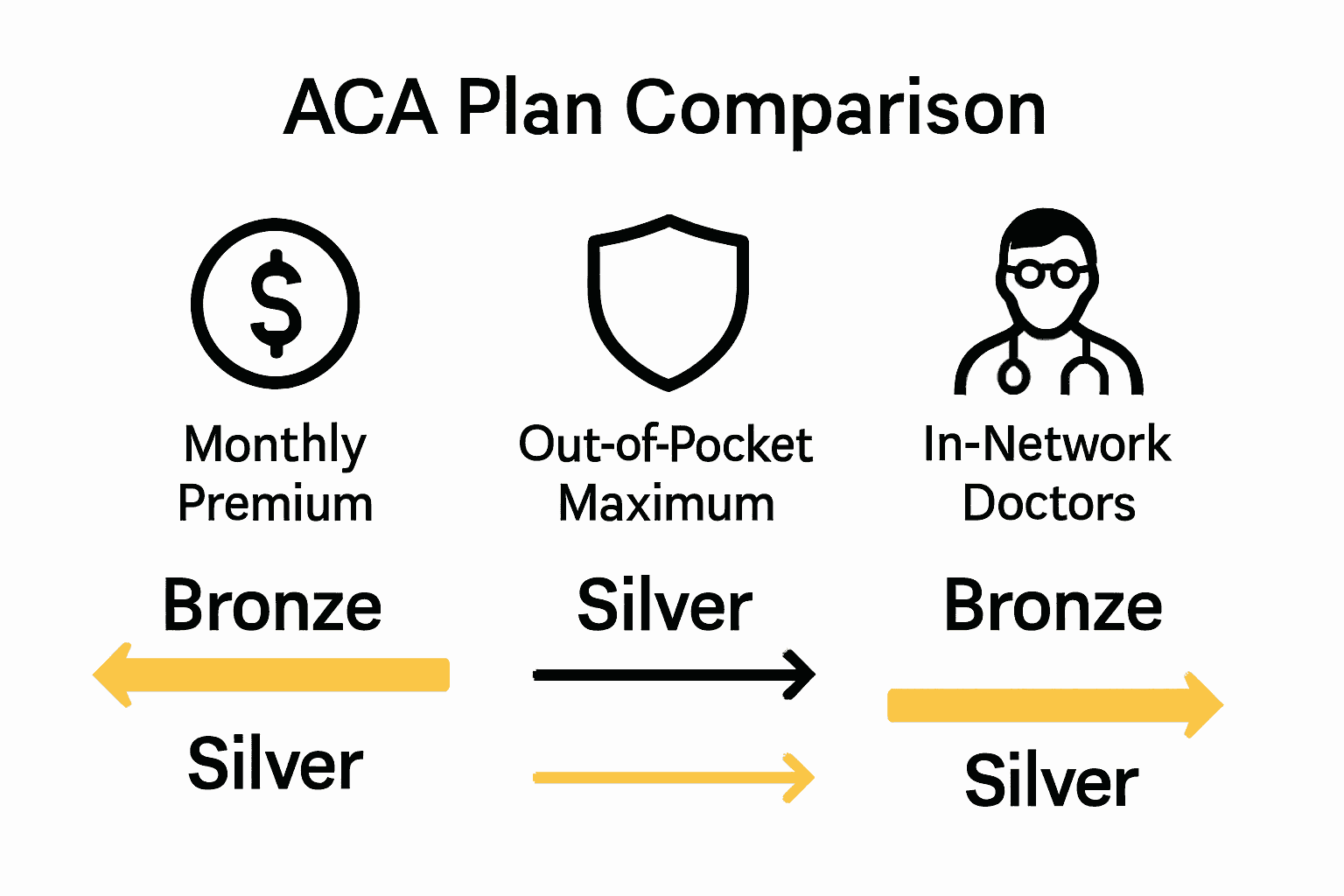

When comparing plans, focus on four key coverage levels bronze, silver, gold, and platinum. Each level offers different cost sharing arrangements between you and the insurance provider. Bronze plans typically have lower monthly premiums but higher out of pocket expenses, while platinum plans offer more comprehensive coverage with higher monthly costs.

Pro Tip: Your income and household size significantly impact your eligibility for premium tax credits and cost sharing reductions.

Dont hesitate to seek assistance. Marketplace Navigators and licensed insurance brokers can provide personalized guidance in identifying plans that match your specific health requirements and budget constraints. They understand the nuanced details that might not be immediately apparent when browsing online.

With a clear understanding of your options, you are now prepared to move forward and evaluate specific plan details that align with your healthcare needs and financial situation.

Step 3: Compare premiums, coverage, and benefits

Comparing ACA health insurance plans goes far beyond simply looking at monthly premiums. Your goal is to find a comprehensive plan that balances affordability with robust healthcare coverage tailored to your family’s specific needs.

According to research from Kaiser Family Foundation, every Marketplace plan must cover ten essential health benefits. However, the devil is in the details when it comes to how those benefits are structured and delivered.

Start by carefully reviewing the Summary of Benefits and Coverage (SBC) for each plan. This document provides a standardized breakdown of what each plan covers and what you will pay. Pay close attention to key financial elements like deductibles, copayments, and out of pocket maximums. Learn how to read insurance quotes clearly to make sure you understand every aspect of potential plans.

Consider your anticipated healthcare usage. If you have ongoing medical conditions or expect frequent medical services, a plan with a higher premium but lower out of pocket costs might save you money in the long run. Conversely, if you are generally healthy, a plan with lower premiums could be more economical.

Pro Tip: Always check if your preferred doctors and healthcare facilities are in the plan’s network to avoid unexpected expenses.

Examine each plan’s prescription drug formulary carefully. Make sure any regular medications you or your family members take are covered and understand the associated costs. Some plans have tiered pricing for prescriptions, which can significantly impact your overall healthcare expenses.

Remember that the cheapest plan is not always the best value. Your ideal plan strikes a balance between affordable premiums, comprehensive coverage, and alignment with your family’s specific healthcare requirements.

Step 4: Evaluate out-of-pocket costs and networks

Understanding the full financial landscape of your health insurance requires a deeper look beyond monthly premiums. Your goal is to comprehensively assess potential healthcare expenses and ensure your preferred medical providers are accessible.

According to research on ACA plans, the maximum out-of-pocket limits for 2025 are $9,200 for individuals and $18,400 for families. The average maximum out-of-pocket (MOOP) cost sits around $8,277, which represents a critical benchmark for evaluating your potential financial exposure.

Start by meticulously checking each plan’s provider network. Get detailed guidance on comparing insurance networks to ensure your current healthcare providers are included. This step is crucial because out-of-network care can dramatically increase your medical expenses.

Consider your specific healthcare needs when assessing networks. If you have established relationships with certain specialists or ongoing treatments, verify their inclusion in the plan. Some plans offer more flexibility with out-of-network care, while others restrict coverage to in-network providers.

Pro Tip: Request a detailed list of in-network providers for any plan you are seriously considering, and cross-reference it with your current healthcare providers.

Evaluate the cost sharing structure carefully. Look beyond the monthly premium to understand copayments, coinsurance, and deductibles. A plan with a lower premium might have significantly higher out-of-pocket costs when you actually need medical services.

Remember that the cheapest plan is not always the most economical. Your ideal plan balances affordable premiums with reasonable out-of-pocket expenses and a network that meets your specific healthcare requirements.

Step 5: Confirm plan selection and enrollment

You are now at the critical moment of transforming your careful research into actual health insurance coverage. The enrollment process might seem complex, but with the right approach, you can complete it smoothly and confidently.

According to research on health insurance enrollment, you have multiple channels for finalizing your plan. You can enroll online through the Marketplace, complete a phone application, submit paper documentation, or work directly with a Navigator or licensed insurance broker who can guide you through each step.

Learn more about enrollment procedures for seniors and families to understand the nuances specific to your situation. Pay special attention to personal details during enrollment to ensure accuracy the smallest error could delay or complicate your coverage activation.

Carefully review all submitted information before final submission. Double check personal details, income information, and selected plan specifics. Most online platforms offer a comprehensive review screen where you can verify every detail before committing.

Pro Tip: Save and screenshot all confirmation documents immediately after enrollment for your personal records.

After enrollment, expect several important communications. Watch for welcome packets, insurance ID cards, and detailed plan documentation. These materials will outline your exact benefits, provide contact information, and explain how to access care under your new plan.

Remember that some plans offer automatic renewal, but it is always wise to actively review and confirm your coverage annually. Healthcare needs change, and what worked perfectly last year might not be the optimal choice for the upcoming period.

Take Charge of Your ACA Health Plan Choices Today

Comparing ACA plans can feel stressful when you want to avoid costly mistakes and protect your loved ones. This article outlined the need to gather the right documents, understand premiums, and evaluate coverage details before enrolling. Many readers worry about selecting an affordable plan that truly fits their healthcare needs for 2025. If you have struggled with confusing networks, complicated benefits, or finding plans that match your budget and current doctors, you are not alone.

Explore our Affordable Health Plans for 2025 collection to simplify your plan comparison even further. See exactly how different options measure up on cost and coverage.

Want to avoid overpaying or missing key benefits during this open enrollment? Visit GenerationHealth.me for expert support, instant quotes, and practical guidance at every step. Make your next health insurance decision with real confidence. Get started now and secure the peace of mind your family deserves.

Frequently Asked Questions

How do I gather personal health details for ACA plan comparisons?

Collect all necessary personal documents like full names, birthdates, and Social Security numbers for every family member applying. This ensures you have accurate information to evaluate potential healthcare subsidies.

What specific factors should I consider when comparing ACA plan premiums?

Focus on the total out-of-pocket costs, including deductibles, copayments, and maximum out-of-pocket limits, alongside monthly premiums. By calculating projected annual costs, you can identify which plans offer the best balance for your healthcare needs.

How can I find which doctors are in-network for my chosen ACA plan?

Check the provider network list included in each plan’s materials, as it details in-network physicians and facilities. Confirm that your current healthcare providers are available under the plan to avoid unexpected expenses, and request an updated list from the insurer if necessary.

What should I do if my prescription medications are not covered by a plan?

Review each plan’s formulary, which outlines covered medications, to determine if your prescriptions are listed. If not, consider a plan that caters to your specific medication needs to avoid higher costs or evaluate alternatives with your healthcare provider.

How can I ensure I’ve correctly completed my ACA plan enrollment?

Double-check all personal information and selected plan details during the enrollment process, making sure everything is accurate. To confirm your submission, save screenshots of confirmation documents, allowing you to reference your enrollment anytime.

When should I start reviewing my ACA plan for the next enrollment period?

Begin reviewing your current ACA plan at least 30 days before the end of the enrollment period. This gives you ample time to assess whether your healthcare needs have changed and to explore new plans that may serve you better.