Did you know that over 14 million Americans rely on Medicare Supplement Plans to help cover healthcare costs that Original Medicare leaves behind? For many seniors, unexpected medical bills can become a major financial concern as they age. Choosing the right supplemental coverage can make a big difference by reducing out-of-pocket expenses and offering peace of mind when visiting healthcare providers across the country.

Key Takeaways

| Point | Details |

|---|---|

| Medicare Supplement Plans (Medigap) | Medigap plans cover out-of-pocket costs not included in Original Medicare, like copayments and deductibles. |

| Standardized Plans | There are ten standardized Medigap plans labeled A through N, offering varying levels of coverage and premium costs. |

| Enrollment Timing | The Medigap Open Enrollment Period allows guaranteed coverage regardless of health status, starting when you turn 65 and enroll in Medicare Part B. |

| Exclusions | Medigap plans do not cover prescription drugs, vision, dental, or long-term care, necessitating separate plans for those needs. |

Table of Contents

- What Is A Medicare Supplement Plan?

- Types Of Medicare Supplement (Medigap) Plans

- How Medigap Works With Original Medicare

- Eligibility And Enrollment Requirements Explained

- Costs, Coverage Gaps, And Key Comparisons

What Is a Medicare Supplement Plan?

A Medicare Supplement Plan, commonly known as Medigap, is a private health insurance designed to fill the coverage gaps left by Original Medicare (Parts A and B). According to the Centers for Medicare & Medicaid Services, these plans help cover out-of-pocket costs like copayments, coinsurance, and deductibles that can quickly add up during medical treatments.

These standardized insurance policies work alongside your Original Medicare coverage, providing additional financial protection. Key features of Medicare Supplement Plans include:

- Coverage across all 50 states when you see Medicare-accepting providers

- Guaranteed renewable policies that cannot be canceled due to health conditions

- Standardized benefits that remain consistent across different insurance companies

Medigap plans are labeled from Plan A through Plan N, with each letter representing a specific combination of benefits. Learn more about Medicare Supplement Plan options to find the coverage that best suits your healthcare needs. While the specific details vary, these plans are designed to provide seniors with predictable healthcare expenses and reduce financial uncertainty during medical treatments.

It’s important to note that Medicare Supplement Plans do not cover prescription drugs, vision, dental, or long-term care. For those additional coverage needs, you might need to explore separate insurance options or Medicare Advantage Plans.

Types of Medicare Supplement (Medigap) Plans

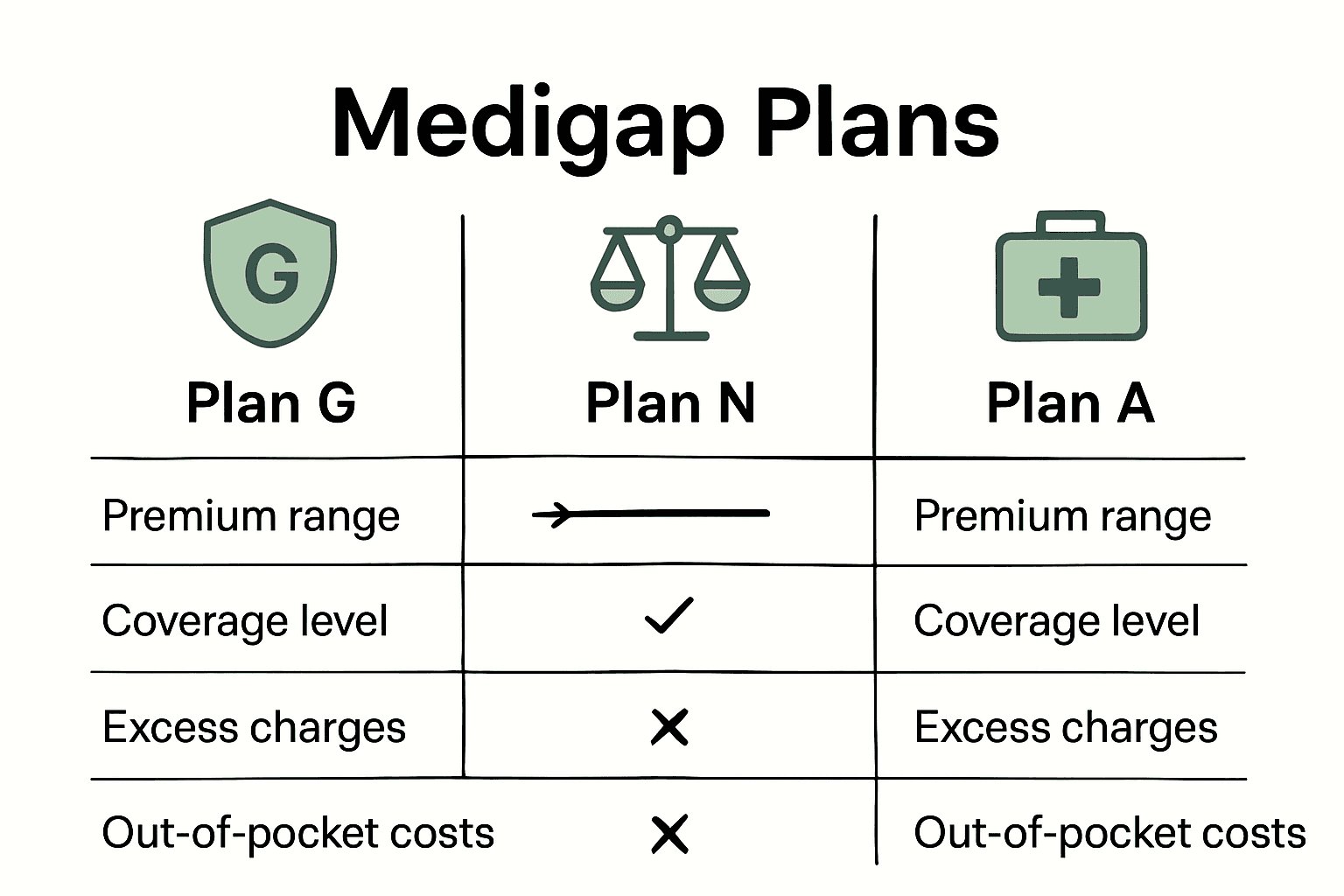

Medicare Supplement Plans are standardized into ten different plans, each labeled with a letter from A to N. These plans offer varying levels of coverage, allowing seniors to choose a plan that best matches their healthcare needs and budget. While the specific benefits are consistent across insurance providers, the monthly premiums can differ significantly.

Most Popular Medigap Plans

Here’s a comparison of popular Medigap plan features:

| Plan | Coverage Level | Monthly Premium Range | Part B Excess Charges | Prescription Drugs |

|---|---|---|---|---|

| Plan G | Most Comprehensive | $120-$250 | Covered | Not Covered |

| Plan N | Moderate-High | $80-$180 | Not Covered | Not Covered |

| Plan A | Basic | $50-$100 | Not Covered | Not Covered |

Some Medicare Supplement Plans are more popular among seniors due to their comprehensive coverage:

- Plan G: Considered the most comprehensive plan, covering nearly all Medicare Part A and B gaps

- Plan N: Offers substantial coverage with slightly lower premiums

- Plan F: Previously the most popular, now only available to those who became Medicare-eligible before January 1, 2020

Plan Coverage Comparison

| Plan Letter | Basic Coverage | Additional Benefits | Popularity |

|---|---|---|---|

| Plan A | Minimal coverage | Limited | Low |

| Plan G | Comprehensive | Extensive | High |

| Plan N | Moderate | Balanced | Medium |

Compare Medicare Supplement Plan details to understand which option might work best for your specific healthcare requirements. Remember that while these plans provide significant additional coverage, they do not include prescription drugs, vision, or dental services.

Choosing the right Medicare Supplement Plan depends on your individual health needs, budget, and anticipated medical expenses. It’s crucial to carefully review each plan’s specific benefits and compare them against your personal healthcare expectations.

How Medigap Works With Original Medicare

Medigap functions as a supplemental insurance policy that works directly alongside Original Medicare, helping to cover the financial gaps in your healthcare expenses. When you receive medical services, Original Medicare (Part A and Part B) pays first, and then your Medicare Supplement Plan steps in to cover remaining costs like copayments, coinsurance, and deductibles.

Coverage Coordination Process

Here’s how the coordination between Original Medicare and Medigap typically works:

- You receive a medical service covered by Medicare

- Original Medicare pays its portion of the approved medical expenses

- Your Medigap policy automatically pays its share of the remaining costs

- You are responsible for any expenses not covered by either plan

Key Advantages of Medigap

- Predictable Costs: Reduces unexpected out-of-pocket medical expenses

- Nationwide Coverage: Works with any healthcare provider that accepts Medicare

- No Network Restrictions: Unlike Medicare Advantage plans, you can see any doctor who accepts Medicare

Important: You must have Medicare Part A and Part B to purchase a Medigap policy.

Explore the differences between Original Medicare and supplemental coverage to understand how these plans work together. Remember that while Medigap provides valuable additional coverage, it does not cover prescription drugs, so you might need a separate Part D plan for medication expenses.

Eligibility and Enrollment Requirements Explained

Medicare Supplement Plans have specific eligibility requirements that can significantly impact when and how you can enroll. The most critical enrollment period is the Medigap Open Enrollment Period, which begins the month you turn 65 and are enrolled in Medicare Part B. During this six-month window, insurance companies cannot deny you coverage or charge higher premiums based on pre-existing health conditions.

Key Enrollment Criteria

To be eligible for a Medicare Supplement Plan, you must meet the following requirements:

- Be 65 years or older

- Enrolled in Medicare Part A and Part B

- Not currently enrolled in a Medicare Advantage Plan

- Reside in the state where you’re purchasing the Medigap policy

Enrollment Timing and Considerations

| Enrollment Period | Coverage Options | Health Screening |

|---|---|---|

| Open Enrollment | Guaranteed Issue | No Medical Screening |

| Outside Open Enrollment | Limited Options | Medical Underwriting |

Discover your Medicare eligibility options to understand the nuances of enrollment. If you miss your initial open enrollment period, you might still be able to purchase a Medigap policy, but insurance companies can use medical underwriting to determine your premiums or potentially deny coverage.

Special circumstances like losing employer health coverage or moving out of your Medicare Advantage Plan’s service area can trigger guaranteed issue rights, which allow you to purchase a Medigap policy without health screenings. Understanding these details can help you make informed decisions about your healthcare coverage.

Costs, Coverage Gaps, and Key Comparisons

Medicare Supplement Plans vary significantly in their monthly premiums and coverage levels, making cost comparison crucial for seniors seeking the most comprehensive and affordable option. The monthly premium for these plans can range from $50 to $300, depending on factors like your age, location, tobacco use, and the specific plan you choose.

Coverage Gap Analysis

Different Medigap plans address coverage gaps differently:

- Plan G: Covers almost all Medicare Part A and B gaps

- Plan N: Offers moderate coverage with lower premiums

- Plan F: Historically most comprehensive, now only available to those Medicare-eligible before 2020

Cost Comparison by Plan

| Plan | Monthly Premium | Part A Deductible | Part B Excess Charges | Out-of-Pocket Maximum |

|---|---|---|---|---|

| Plan G | $120-$250 | Fully Covered | Fully Covered | $0 |

| Plan N | $80-$180 | Partially Covered | Not Covered | $20-$50 |

| Plan A | $50-$100 | Not Covered | Not Covered | Limited |

Understand how to read insurance quotes effectively to make an informed decision about your Medicare Supplement Plan. While cost is important, consider your personal health needs, expected medical expenses, and potential future healthcare requirements when selecting a plan.

Remember that premiums can increase annually, and the cheapest plan today might not be the most cost-effective option in the long run. Carefully evaluate each plan’s benefits, potential out-of-pocket expenses, and how well they align with your specific healthcare needs.

Feel Confident Choosing the Right Medicare Supplement Plan

Are you overwhelmed by the confusing landscape of Medicare Supplement (Medigap) options? This article explained the different plan types, outlined the enrollment rules, and stressed the importance of comparing benefits and costs. But choosing the right Medigap plan still feels risky when you are worried about surprise bills, complex coverage gaps, and finding answers you can trust. Even a small mistake could mean paying more or missing out on the medical care you need in the future.

Compare real-world plan details and see how your situation matches up to what others have faced. GenerationHealth.me stands by your side with step-by-step guidance, clear cost comparisons, and ongoing education for every stage of your Medicare journey.

Take control of your healthcare decisions today. Visit GenerationHealth.me for instant quotes, expert advice, and answers to your most pressing coverage questions. Start exploring now so you can secure the Medigap protection you deserve and avoid costly mistakes in the future.

Frequently Asked Questions

What is a Medicare Supplement Plan?

A Medicare Supplement Plan, or Medigap, is a private insurance designed to cover out-of-pocket costs not fully paid by Original Medicare (Parts A and B).

How do Medigap plans work with Original Medicare?

Medigap plans complement Original Medicare by covering remaining costs like copayments and deductibles after Medicare pays its share for medical services.

What are the main types of Medicare Supplement Plans?

There are ten standardized Medigap plans labeled from A to N, each offering varying levels of coverage. Popular plans include Plan G, Plan N, and Plan F.

What eligibility criteria must I meet to enroll in a Medigap policy?

To enroll in a Medigap policy, you must be 65 or older, enrolled in Medicare Part A and Part B, and reside in the state where you plan to purchase the policy.