Table of Contents

- What Is Open Enrollment And Why Does It Exist?

- The Importance Of Enrolling In Health Plans

- Understanding Your ACA Marketplace Options

- Medicare Advantage Plans And Open Enrollment

- The Impact Of Missing Open Enrollment Periods

Quick Summary

| Takeaway | Explanation |

|---|---|

| Understand open enrollment periods | Open enrollment allows you to enroll in health insurance without restrictions once a year, usually lasting several weeks. |

| Review options before enrolling | Compare health plans, assess coverage needs, and identify any changes during the open enrollment period to make informed decisions. |

| Missing enrollment has consequences | If you miss the open enrollment period, you may face gaps in coverage and higher costs until the next opportunity arises. |

| Medicare Advantage offers more choices | Medicare Advantage plans combine multiple benefits into one plan, including additional services beyond original Medicare, making comparison during open enrollment crucial. |

| Plan for special enrollment opportunities | Certain life events allow for enrollment outside the open period, making it important to know your options to maintain health coverage. |

What is Open Enrollment and Why Does it Exist?

Open enrollment is a specific annual period when individuals can select or modify their health insurance coverage without facing typical enrollment restrictions. Unlike other times of the year, this window allows you to sign up for new plans, switch providers, or adjust existing coverage without requiring a qualifying life event.

Understanding the Fundamental Purpose

Healthcare.gov defines open enrollment as a structured mechanism designed to maintain balance in health insurance markets. The primary goal is preventing what insurers call “adverse selection” – a scenario where only sick individuals seek coverage, which would dramatically increase overall healthcare costs.

The concept works like an annual reset button for health insurance. By creating a predictable timeframe, insurance companies can:

- Calculate risk more accurately

- Stabilize premium pricing

- Ensure fair coverage opportunities for all participants

- Prevent last-minute healthcare coverage gaps

How Open Enrollment Protects Consumers and Insurers

Open enrollment periods serve as a critical protection mechanism for both consumers and insurance providers. For individuals, it guarantees an opportunity to reassess healthcare needs, compare plan options, and make informed decisions without bureaucratic barriers.

For insurance companies, these designated windows help manage financial risks by creating a structured environment where healthy and less healthy individuals enter the risk pool simultaneously. This approach prevents scenarios where people would only purchase insurance when they anticipate immediate medical expenses.

Typically, open enrollment periods last several weeks, during which individuals can:

- Review current health insurance coverage

- Explore alternative plan options

- Make changes to existing health insurance

- Add or remove dependent coverage

- Select supplemental insurance products

Missing the open enrollment window means waiting until the next annual period or experiencing a significant life change that triggers a special enrollment period. Planning ahead and understanding these windows can save you from unexpected coverage challenges.

The Importance of Enrolling in Health Plans

Health insurance plays a critical role in protecting your physical and financial wellbeing. Having comprehensive coverage means more than just accessing medical treatments when needed – it represents a strategic approach to managing personal health risks and potential financial challenges.

Financial Protection and Risk Management

Centers for Disease Control research highlights that uninsured individuals face significantly higher risks of financial instability due to unexpected medical expenses. Without health insurance, a single serious medical event can potentially bankrupt an individual or family.

The financial implications of being uninsured extend far beyond immediate medical costs. Individuals without health coverage often experience:

- Higher out-of-pocket expenses for basic medical treatments

- Limited access to preventive care services

- Potential long-term financial strain from untreated medical conditions

- Increased likelihood of medical debt

Comprehensive Healthcare Access

Health insurance provides more than financial security. It creates a pathway to comprehensive healthcare that supports ongoing wellness and early intervention. Learn more about ACA health insurance strategies to understand how different plans can meet your specific healthcare needs.

Modern health plans typically offer coverage that includes:

- Annual preventive screenings

- Regular check-ups with primary care physicians

- Access to specialist consultations

- Prescription medication coverage

- Mental health and wellness services

By enrolling in a health plan during open enrollment, you’re not just purchasing insurance – you’re investing in your long-term health and creating a safety net that protects both your physical and financial future. Proactive enrollment ensures you have continuous coverage tailored to your evolving healthcare requirements.

Understanding your ACA Marketplace Options

The Affordable Care Act (ACA) Marketplace provides a structured platform where individuals and families can explore, compare, and purchase health insurance plans that meet their specific needs. This government-created marketplace offers a transparent, standardized approach to selecting health coverage.

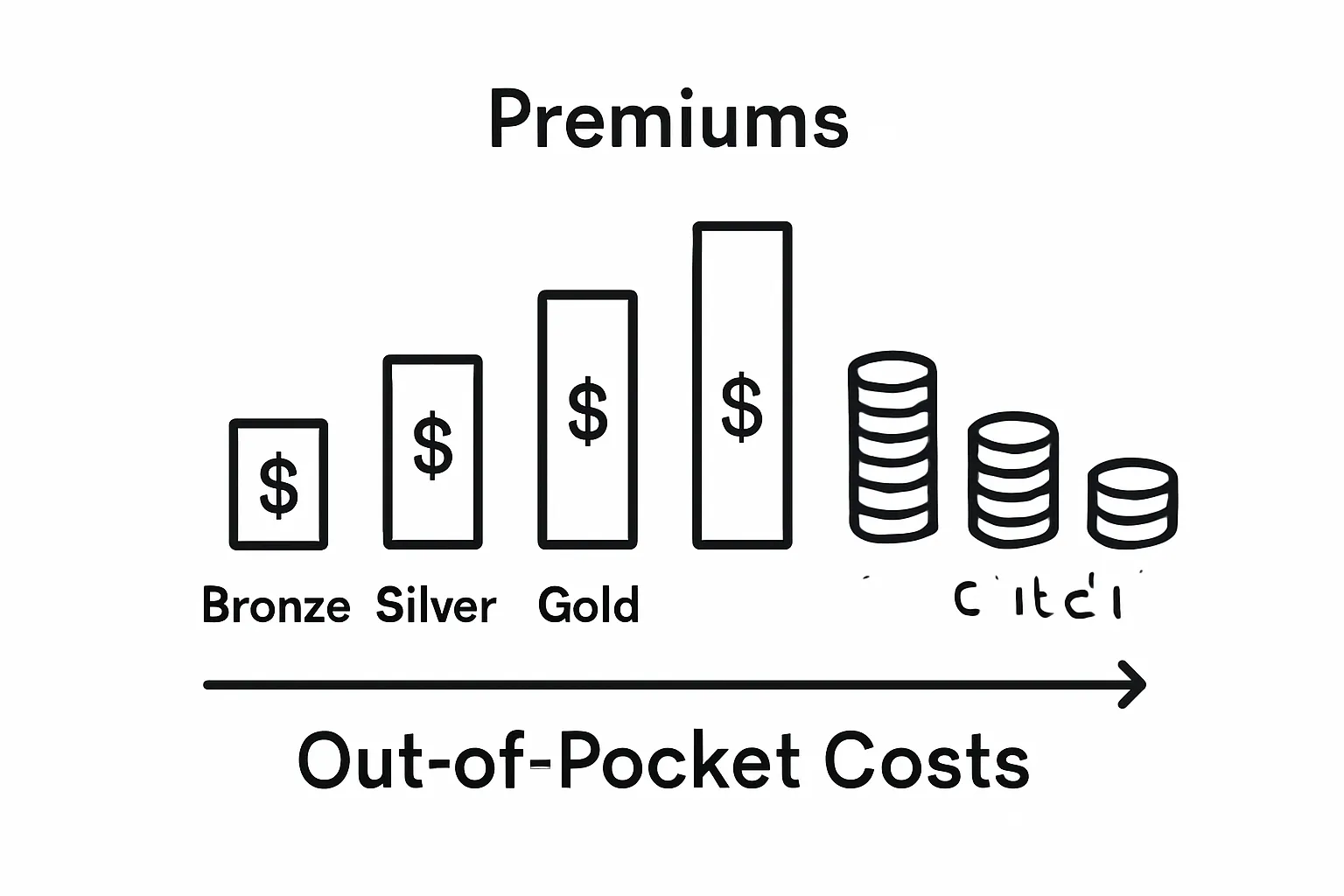

Marketplace Plan Categories

Healthcare.gov explains that ACA Marketplace plans are categorized into four primary metal tiers: Bronze, Silver, Gold, and Platinum. Each tier represents a different balance between monthly premiums and out-of-pocket expenses.

Here is a comparison of ACA Marketplace plan categories to help you quickly understand differences in costs and coverage options.

| Plan Category | Premium Costs | Out-of-Pocket Costs | Key Feature |

|---|---|---|---|

| Bronze | Lowest | Highest | Best for lower premiums, higher costs when care needed |

| Silver | Moderate | Moderate | Balanced cost-sharing, eligible for extra savings |

| Gold | High | Low | Higher premiums, lower out-of-pocket expenses |

| Platinum | Highest | Lowest | Best for frequent care, highest monthly premium |

These plan categories help consumers understand potential healthcare costs:

- Bronze plans: Lowest monthly premiums, highest out-of-pocket costs

- Silver plans: Moderate premiums and out-of-pocket expenses

- Gold plans: Higher monthly premiums, lower out-of-pocket costs

- Platinum plans: Highest monthly premiums, lowest out-of-pocket expenses

Eligibility and Financial Assistance

Understand your eligibility for ACA Marketplace coverage to determine which plans you might qualify for. Most individuals can access Marketplace plans, with financial assistance available based on income levels.

Key factors influencing Marketplace plan eligibility include:

- Household income

- Family size

- Citizenship or legal residency status

- Age

- Current health insurance coverage

The ACA Marketplace offers significant advantages, including guaranteed coverage regardless of pre-existing conditions, comprehensive essential health benefits, and potential premium tax credits. By carefully comparing options during open enrollment, you can find a plan that provides robust coverage while managing your healthcare expenses effectively.

Medicare Advantage Plans and Open Enrollment

Medicare Advantage plans offer an alternative approach to traditional Medicare coverage, providing comprehensive healthcare options for seniors and eligible individuals. These plans, offered by private insurance companies, combine Medicare Part A and Part B benefits into a single, integrated package.

Understanding Medicare Advantage Basics

Medicare.gov defines Medicare Advantage plans as comprehensive health coverage options that often include additional benefits not available through original Medicare. These plans typically provide more extensive coverage and can include prescription drug, dental, vision, and hearing services.

Key characteristics of Medicare Advantage plans include:

- Comprehensive coverage beyond original Medicare

- Potential lower out-of-pocket costs

- Additional wellness and preventive care benefits

- Prescription drug coverage often included

- Network-based healthcare services

Open Enrollment Opportunities

How to Maximize Medicare Coverage explains that the annual Medicare Advantage open enrollment period provides a critical window for beneficiaries to review and adjust their healthcare coverage. This period allows individuals to:

- Switch between Medicare Advantage plans

- Return to original Medicare

- Add or modify prescription drug coverage

- Explore plans with better cost structures or additional benefits

The open enrollment period typically runs from October 15 to December 7 each year, offering a structured opportunity to reassess healthcare needs. Seniors can compare plan options, evaluate changing health requirements, and select coverage that provides the most comprehensive and cost-effective protection for their unique medical circumstances.

The Impact of Missing Open Enrollment Periods

Missing open enrollment periods can have significant consequences for your healthcare coverage and financial security. When you fail to enroll or make necessary changes during these designated windows, you potentially expose yourself to substantial risks and limitations in healthcare access.

Coverage Limitations and Restrictions

Healthcare.gov indicates that missing open enrollment typically means waiting until the next annual period to obtain or modify health insurance. This delay can create critical gaps in healthcare protection that may have long-lasting implications.

Potential consequences of missing open enrollment include:

- Inability to change or select new health insurance plans

- Potential lack of coverage for essential medical services

- Higher out-of-pocket expenses for medical treatments

- Limited options for addressing changing healthcare needs

Special Enrollment Considerations

Learn more about senior enrollment options to understand exceptions and alternatives. While standard open enrollment periods are strict, certain life events can trigger special enrollment opportunities.

Qualifying life events that might allow enrollment outside standard periods typically include:

- Marriage or divorce

- Birth or adoption of a child

- Loss of existing health coverage

- Significant changes in household income

- Relocation to a new service area

Proactively managing your healthcare enrollment is crucial. By understanding open enrollment timelines and potential exceptions, you can avoid unexpected coverage gaps and ensure continuous, comprehensive health protection.

The table below outlines common qualifying life events that may grant a Special Enrollment Period, helping you determine if you might still have enrollment options outside open enrollment.

| Qualifying Life Event | Description |

|---|---|

| Marriage or divorce | Getting married or divorced may allow for plan changes |

| Birth or adoption of a child | Adding a child to your household enables special enrollment |

| Loss of existing coverage | Losing employer or government coverage qualifies you |

| Change in household income | Significant increases or decreases may affect eligibility |

| Relocation | Moving to a new area can trigger a new enrollment window |

Take Control During Open Enrollment with Expert Guidance

Missing the open enrollment period can leave you unprotected, facing confusing choices or higher out-of-pocket costs. This article highlights the stress and uncertainty that comes from confusing health plan options, unpredictable coverage gaps, and the fear of missing out on essential benefits for your family. Open enrollment is your key opportunity to secure coverage that truly fits your needs and brings peace of mind.

If you are navigating Medicare or Marketplace coverage, our resources can help. Explore our Medicare & Seniors-Insurance Agents section to get clear, step-by-step answers for your specific situation. If you need help understanding if you qualify for Marketplace plans, browse our Eligibility for ACA Marketplace resources for up-to-date tips and strategies.

Do not let another enrollment window pass you by. Visit GenerationHealth.me today and get instant quotes, expert support, and a personalized enrollment experience. Make confident decisions about your healthcare coverage now—so you are ready for anything ahead.

Frequently Asked Questions

What is open enrollment?

Open enrollment is an annual period during which individuals can select or modify their health insurance coverage without needing a qualifying life event.

Why is open enrollment important for health insurance?

Open enrollment is crucial because it allows consumers to reassess their healthcare needs, compare plan options, and make informed decisions about their health insurance without bureaucratic barriers.

What happens if I miss the open enrollment period?

Missing the open enrollment period can limit your options, preventing you from obtaining or modifying health insurance until the next annual enrollment period unless you qualify for a special enrollment period due to significant life changes.

What are the benefits of enrolling during open enrollment?

Enrolling during open enrollment ensures you have continuous coverage tailored to your evolving health needs, access to essential medical services, and financial protection against unforeseen medical expenses.