Table of Contents

- What Are Insurance Quotes And Why They Matter

- Key Components Of Insurance Quotes Explained

- Interpreting Premiums, Deductibles, And Copayments

- How Coverage Options Affect Your Insurance Quote

- Tips For Comparing Insurance Quotes Effectively

Quick Summary

| Takeaway | Explanation |

|---|---|

| Understand your insurance quotes | Insurance quotes provide estimated costs for coverage and help in financial decision-making. |

| Compare multiple insurance quotes | Gathering quotes from various providers helps identify the best coverage options and potential savings. |

| Focus on key quote components | Recognize premium, deductible, coverage limits, and copayments in quotes to assess financial commitment effectively. |

| Consider additional factors beyond price | Analyze total out-of-pocket expenses, provider networks, and hidden costs when evaluating different insurance plans. |

| Choose coverage wisely based on needs | Tailor your insurance plans according to personal health needs and financial capabilities for optimal care. |

What Are Insurance Quotes and Why They Matter

An insurance quote is a critical financial document that provides potential customers with an estimated cost of insurance coverage before they commit to purchasing a policy. Understanding insurance quotes allows you to make informed decisions about protecting your health, property, and financial future.

The Fundamental Purpose of Insurance Quotes

Insurance quotes serve as preliminary price estimates that help consumers compare different coverage options. When you request a quote, insurance providers analyze specific details about your personal circumstances to calculate potential premium costs. These details might include:

- Your age

- Health history

- Geographic location

- Specific coverage needs

- Risk factors relevant to the type of insurance

Breaking Down How Quotes Work

Quotes are not permanent pricing commitments but rather detailed predictions based on the information you provide. Insurance companies use complex algorithms and risk assessment models to generate these estimates. Accuracy matters, so providing complete and honest information ensures you receive the most precise quote possible.

The quoting process typically involves answering a series of questions about your personal circumstances, health status, or asset details. Each piece of information helps insurers assess potential risk and determine appropriate pricing. For Medicare, ACA Marketplace, dental, and vision plans, these quotes can vary significantly based on individual factors.

Why Comparing Quotes Matters

Comparing multiple insurance quotes allows you to find the most suitable and affordable coverage for your specific needs. By obtaining quotes from different providers, you can:

- Identify the most cost-effective options

- Understand varying coverage levels

- Recognize potential discounts

- Make an informed financial decision

Remember that the lowest quote isn’t always the best choice. Consider coverage quality, provider reputation, and long-term value when making your selection.

Key Components of Insurance Quotes Explained

Insurance quotes are complex documents that contain multiple essential elements determining your coverage and potential costs. According to the National Association of Insurance Commissioners, understanding these components helps you make informed insurance purchasing decisions.

Core Quote Components

Each insurance quote includes several critical details that collectively determine your coverage and premium. Core quote components typically represent a comprehensive overview of your potential insurance plan:

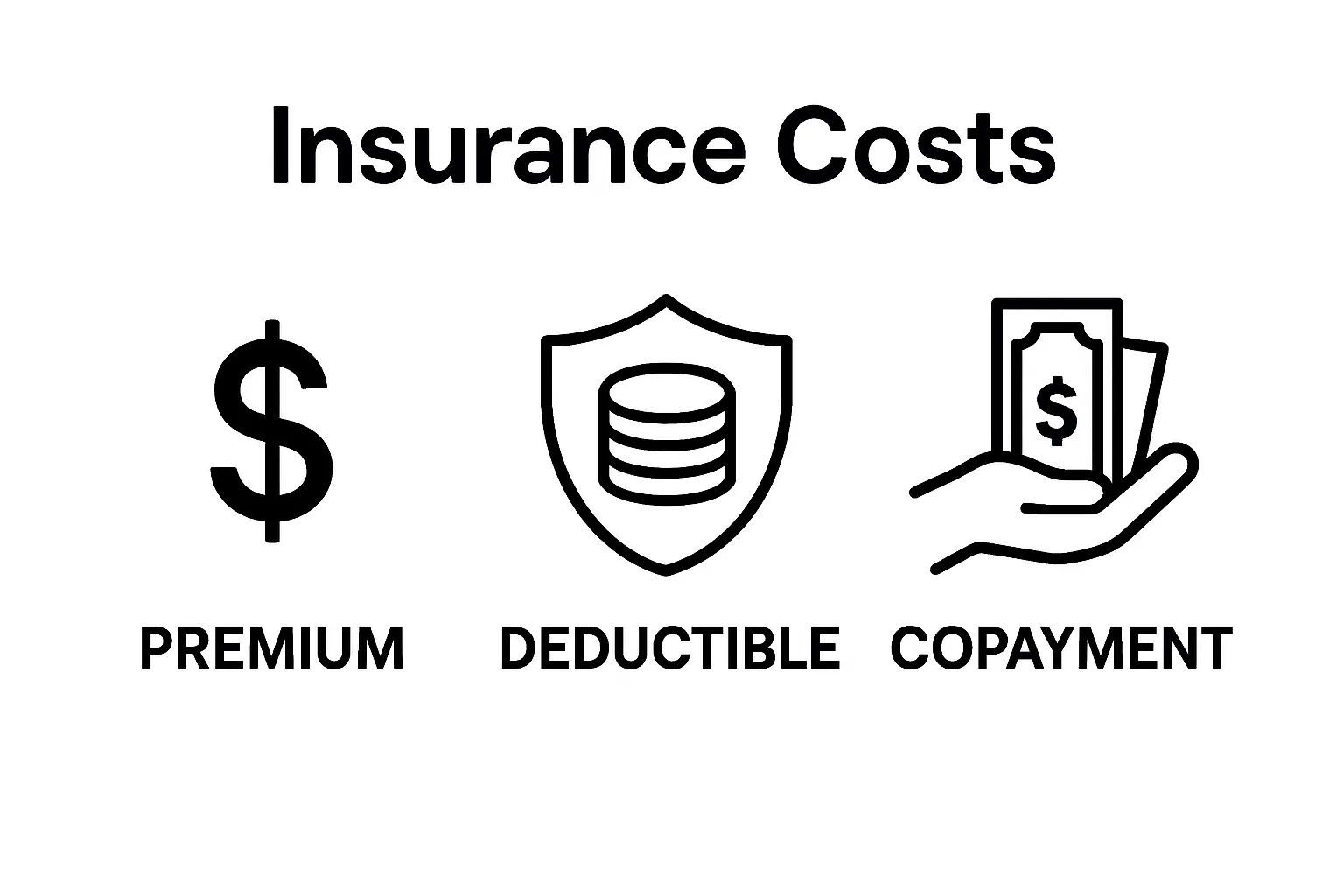

- Premium: The amount you pay regularly for insurance coverage

- Deductible: Your out-of-pocket expense before insurance begins covering costs

- Coverage Limits: Maximum amount the insurance company will pay

- Copayments: Fixed amounts you pay for specific services

- Coinsurance: Percentage of costs you share with the insurance provider

Detailed Coverage Analysis

Insurance quotes provide nuanced information about potential financial protection. For older adults exploring Medicare, ACA Marketplace, dental, or vision plans, these details become increasingly important. Each quote element reflects specific risk assessments and financial calculations performed by insurance providers.

The premium represents your primary financial commitment, calculated based on multiple factors including age, health status, location, and desired coverage level. Younger individuals typically receive lower premiums, while those with more complex health histories might encounter higher rates.

Understanding Quote Variations

Quotes can vary significantly between providers, even for seemingly identical coverage. Careful comparison becomes crucial in identifying the most appropriate plan. Factors influencing quote variations include:

- Individual health profile

- Geographic region

- Specific insurance provider’s risk assessment models

- Current market conditions

- Available discounts or promotional offers

By thoroughly examining each quote component, you can make a strategic decision that balances comprehensive coverage with financial feasibility.

Remember that the cheapest quote is not always the most beneficial option.

Remember that the cheapest quote is not always the most beneficial option.

Interpreting Premiums, Deductibles, and Copayments

Medicare and health insurance systems involve complex financial structures that require careful understanding. These three key financial components determine how you interact with your insurance coverage and manage healthcare expenses.

Understanding Insurance Premiums

Premiums represent the regular payment you make to maintain active insurance coverage. Think of this as your membership fee that keeps your insurance policy active. For seniors and families exploring Medicare or ACA Marketplace plans, premium costs can vary dramatically based on:

- Age

- Location

- Selected coverage level

- Income

- Health status

Typically, you pay premiums monthly, quarterly, or annually. Lower premiums often mean higher out-of-pocket expenses when receiving medical services, while higher premiums might offer more comprehensive coverage.

Decoding Deductibles

A deductible is the amount you pay for covered healthcare services before your insurance plan starts to pay. Imagine a deductible as your personal financial responsibility before insurance kicks in. For instance, if your plan has a $1,500 deductible, you would pay the first $1,500 of covered medical expenses entirely out of pocket.

Deductible amounts significantly impact your overall healthcare spending. Higher deductible plans usually have lower monthly premiums, while lower deductible plans provide more immediate coverage but cost more monthly.

Navigating Copayments

Copayments are fixed amounts you pay for specific medical services after meeting your deductible. These predictable costs help you budget for healthcare expenses. A typical copayment might be $20 for a doctor’s visit or $10 for a prescription.

Understanding how copayments work can help you:

- Predict medical expenses

- Compare different insurance plans

- Budget for healthcare costs

- Choose providers strategically

Remember that copayments, premiums, and deductibles work together to determine your total healthcare spending. Carefully analyzing these components helps you select the most financially sensible insurance plan for your specific needs.

The table below breaks down and defines the key financial components you will encounter in any insurance quote to help you quickly understand what each term means.

| Component | Definition |

|---|---|

| Premium | Regular payment made to maintain active insurance coverage |

| Deductible | Amount you pay out-of-pocket before insurance begins to cover costs |

| Copayment | Fixed amount you pay for specific medical services after meeting your deductible |

| Coinsurance | Percentage of costs you share with your insurance provider after meeting your deductible |

| Coverage Limit | Maximum amount your insurance will pay for covered services |

How Coverage Options Affect Your Insurance Quote

Insurance coverage options play a critical role in determining the final cost and structure of your insurance quote. Understanding these nuanced choices helps you balance comprehensive protection with financial feasibility.

Core Coverage Level Considerations

Insurance coverage options directly influence your quote’s financial framework. Different coverage levels create substantial variations in pricing and protection. These options typically include:

- Basic coverage with minimal protection

- Comprehensive plans with extensive medical services

- Specialized plans targeting specific health needs

- High deductible plans with lower monthly premiums

- Low deductible plans with higher monthly costs

Impact of Coverage Choices

Choosing your coverage level involves strategic trade-offs between monthly expenses and potential out-of-pocket costs. A more extensive plan might include additional services like vision, dental, or prescription drug coverage, which increases your premium but potentially reduces long-term healthcare expenses.

For seniors exploring Medicare or ACA Marketplace plans, understanding these trade-offs becomes crucial. Learn more about navigating these choices in our guide to getting started with ACA health insurance.

Customizing Your Protection

Personalized coverage options allow you to tailor insurance quotes to your specific health requirements. Factors influencing these customizations include:

- Current health status

- Anticipated medical needs

- Family medical history

- Budget constraints

- Preferred healthcare providers

Remember that the most expensive quote is not always the most comprehensive, and the cheapest option might leave significant gaps in your healthcare protection. Carefully evaluate each option to find the optimal balance between cost and coverage.

This table summarizes how different coverage choices impact both your monthly insurance costs and your potential out-of-pocket spending, helping you weigh the key trade-offs when customizing your insurance options.

| Coverage Choice | Monthly Premium | Out-of-Pocket Costs | Typical Features |

|---|---|---|---|

| Basic Coverage | Lower | Higher | Minimal protection, higher deductibles, fewer services |

| Comprehensive Plan | Higher | Lower | Extensive services, lower deductibles, added benefits |

| High Deductible Plan | Lower | Higher until deductible | Lower premium, higher up-front cost-sharing, good for low usage |

| Low Deductible Plan | Higher | Lower up-front | Higher premium, lower cost before insurance pays |

| Specialized Plan | Varies | Varies | Tailored to specific needs (e.g., vision, dental, prescription) |

Tips for Comparing Insurance Quotes Effectively

Comparing insurance quotes requires a strategic approach to ensure you find the most appropriate coverage for your specific needs. Developing a systematic method helps you navigate the complex landscape of insurance options.

Establishing Comparison Criteria

Before diving into multiple quotes, establish clear comparison criteria that go beyond simple price considerations. Effective comparison involves evaluating multiple dimensions of potential insurance plans:

- Total potential out-of-pocket expenses

- Network of healthcare providers

- Specific coverage details

- Prescription drug coverage

- Additional wellness benefits

Analyzing Hidden Cost Factors

Beyond the visible premium and deductible, several hidden cost factors can significantly impact your overall healthcare expenses. Some critical elements to investigate include copayment structures, annual maximum out-of-pocket limits, and potential additional fees.

For seniors exploring Medicare or ACA Marketplace plans, understanding the role of insurance brokers can provide additional insights into navigating complex quote comparisons.

Technical Comparison Strategies

To compare quotes effectively, create a standardized worksheet that allows side-by-side evaluation. This approach helps you objectively assess different insurance options by:

- Documenting each quote’s key financial components

- Highlighting unique plan features

- Tracking potential additional benefits

- Comparing provider networks

- Noting potential limitations

Remember that the most expensive quote is not always the most comprehensive, and the cheapest option might leave significant gaps in your healthcare protection. Carefully evaluate each option to find the optimal balance between cost, coverage, and personal healthcare needs.

Ready to Make Sense of Insurance Quotes? We Can Help

Trying to decode insurance quotes can feel overwhelming. If you have ever been confused by premiums, deductibles, or uncertain about which plan truly fits your needs, you are not alone. Many people worry about hidden costs and missing out on the right coverage. When you want straightforward guidance on reading quotes, GenerationHealth.me is your trusted partner.

Discover a simpler way to compare plans, understand your options clearly, and gain confidence in your choices. Visit our Medicare & Seniors-Insurance Agents page for expert support that makes navigating coverage choices much easier. Take control of your health insurance decisions today by visiting GenerationHealth.me for instant quotes and personalized help. Do not wait—start your journey toward clarity and affordable coverage now.

Frequently Asked Questions

What is an insurance quote?

An insurance quote is an estimated cost of insurance coverage that providers offer to potential customers based on specific personal details, helping them to make informed decisions about purchasing a policy.

Why is it important to compare multiple insurance quotes?

Comparing multiple insurance quotes allows consumers to identify cost-effective options, understand varying coverage levels, recognize potential discounts, and ultimately make an informed financial decision about their insurance needs.

What key components should I look for in an insurance quote?

When reviewing an insurance quote, focus on the premium, deductible, coverage limits, copayments, and coinsurance. These elements will determine your coverage and overall costs.

How can I ensure that my insurance quote is accurate?

To receive an accurate insurance quote, provide complete and honest information regarding your age, health history, geographical location, and coverage needs when completing the quoting process.

Recommended

- Understanding the Role of Insurance Agents in Healthcare – GenerationHealth.Me Your Online Health Insurance Marketplace

- Complete Vision Plan Enrollment Guide for Adults 64+ – GenerationHealth.Me Your Online Health Insurance Marketplace

- Understanding the Role of Brokers in Medicare – GenerationHealth.Me Your Online Health Insurance Marketplace